Take a look at Twitter, and you will see never-ending debates on whether startups or MNCs are the best.

Having worked in both, here are my 2 cents.

MNCs or established, large companies might be the better option for you if you want:

Higher pay: Big companies are willing to pay the best of the best for talent

Better job security: They have been in the business for a longer time and are more stable

Well equipped work space: They have the money to invest in the best tools and resources needed for upgrading your work

Better perks: Health benefits, freebies

Cons:

Office politics: This was the worst part for me.

Feeling undervalued: There are a lot of employees, and it is practically impossible for the higher order to listen to everyone. Your opinions or inputs tend to be given less importance.

Not flexible: Most of the companies want you to stick to their rules. Employees are rarely consulted on what *they* want.

Startups or smaller companies might be the better option if you want:

More job satisfaction: The pride you feel when your company is growing is unmatched. You played a role in it, and that is a huge achievement.

Less office politics

A tightly-knit workspace where everyone is easily reachable including the CEO

A job where you are valued

Cons:

Lesser pay: Small companies can hardly compete with MNCs when it comes to offering the best pay package

High pressure: Lots of work, less work-life balance

Cash-strapped: Hardly any freebies; access only to those tools that are absolutely essential for your work

Of course, this does not apply to all the MNCs and Startups out there. Each one is different. But from my experience, this is what I have encountered.

Honestly, I feel everyone should try both at least once to see what it is like.

Then go the Marie Kondo way perhaps – choose the one that sparks joy.

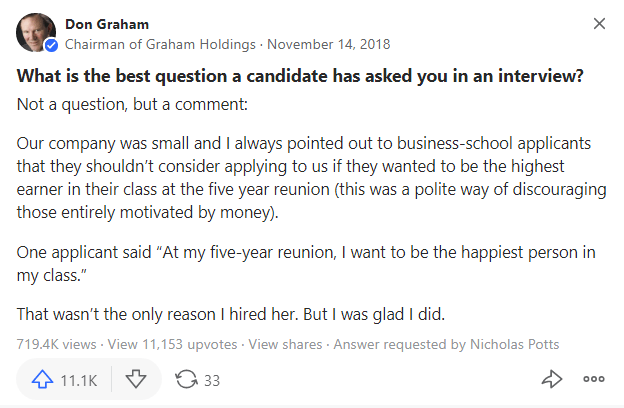

To finish this off, posting a snippet I saw on Quora. It made me smile.

It goes without saying that our screen time has doubled (maybe even tripled) after COVID-19 induced lockdowns and quarantines. All that time indoors has made us reach for our devices. So it is not surprising when studies indicate our eye problems have worsened in the last one year or so.

For someone who is working in the field of Information Technology, spending a lot of time staring at the screen is nothing new.

But there is another problem – I love reading.

Physical copies are expensive, and there was a storage problem at home, so I had resorted to using the Kindle app. It was highly convenient. I loved it. But then the eye strain began. Dryness and a heavy feeling above my eyelid. I knew this was happening because of all the phone reading, because when I stopped, the discomfort would subside.

I realized it was time to finally invest in a Kindle.

For someone who loved reading so much, why didn’t I pick up a popular e-reader like the Kindle sooner?

I am frugal. I don’t buy something unless I am absolutely convinced that it would add some kind of value to my life. The reason why I wasn’t convinced is the next point.

I never knew Kindle was anti-glare& easy-on-the-eyes. All I heard from fellow readers was about its space-efficiency. Yes, storage was a problem at home, but that was not a serious concern for me, which leads us to the third point.

I was ignorant. I did not know the benefits of using a Kindle. I did not bother looking too much into it, because a) it wasn’t cheap b) mentioned in the next point.

I was truly happy with my Kindle app. Everything a Kindle could do, my Kindle app was able to do perfectly. The app could even highlight in colors, something the Kindle device could not do. So why even bother?

I am sure there are more, but these are the reasons at the top of my head.

A couple of days back, I finally succumbed and got this Kindle.

In just a day, my eye strain considerably reduced. I do not feel any heaviness or pain. I think I even shed a few happy tears over how relaxed my eyes feel now.

A few reasons why I got the Kindle Oasis.

I initially thought of getting the basic model. But through some research, I realized it is best to invest in an e-reader that offers at least 300 ppi resolution (for sharp text). The basic Kindle model has 167 ppi.

I thought of going for the Paperwhite next. This model generally has the best reviews. It was a close call, but what made me finally get the Oasis was the a) warm, adjustable light b) the page buttons c) a fantastic Amazon Prime Day sale!

I find the warm light really helpful & relaxing for night time reading. The page buttons are okay, but I would have been fine even without them. That said, if there wasn’t a sale going on, I would have gone for the Paperwhite.

An investment for the eyes. That’s how I would prefer to look at it.

A Family Adventure with Tata Nano. Picture Courtesy: Wikimedia Commons

When the Tata Nano came out, I remember looking at the owners in awe.

They had the guts to own the cheapest car in India.

Society doesn’t treat you well when they know you haven’t paid a huge sum for something – be it a car, house, TV, anything.

Nano owners knew that – “Yes this is a cheap car. My relatives, friends and family might gossip behind my back. But guess what? It doesn’t matter!”

Similarly, ever told someone that you plan on buying a studio apartment? Try and gauge their reaction to see how deeply embedded materialism is.

You need a high level of emotional stability and strength to own something that isn’t a status symbol. Most are only talk “I don’t give a f***” but Nano owners truly proved it with their actions! They really didn’t give a f***.

Their only wish was to transport themselves and their family from point A to B in a new car they can truly call their own.

No other frills.

Plain and simple.

It is another thing that Tata Nano did not live up to its expectations because of the cheap material used, resulting in its downfall. It was discontinued in April 2019.

Nevertheless, because of Tata Nano, I came to admire this different group of people and their persona.

If you are/were a Tata Nano owner, hats off to you! For showing everyone around how comfortable you’re in your own skin, without the need to prove a point to anyone.

The cheapest way to learn is by analyzing other people’s mistakes.

True, sometimes you need to make your own mistakes. It is only then that the lesson sticks to you. But that can get quite expensive, in terms of time and capital. This is why I feel, more than success stories, you need to observe and learn from other people’s failures. They teach you a lot, with no damages incurred.

I love going through Quora and Reddit. Back in the day, we used to have Yahoo! Answers. You get to learn from the insightful answers given by users who truly want to help you out without any monetary gain.

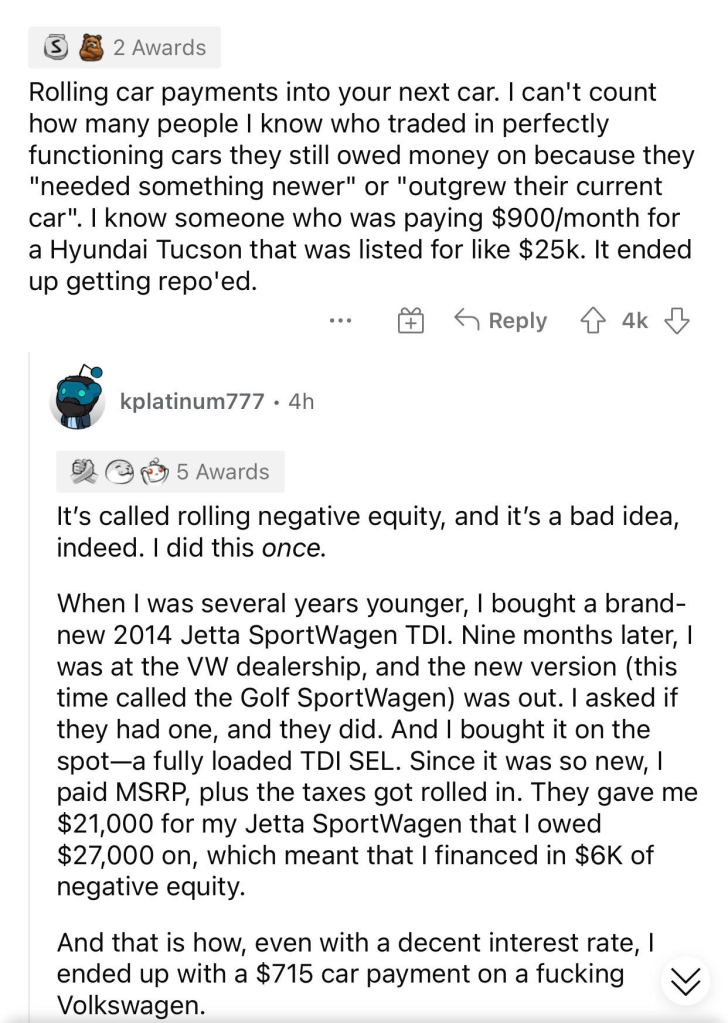

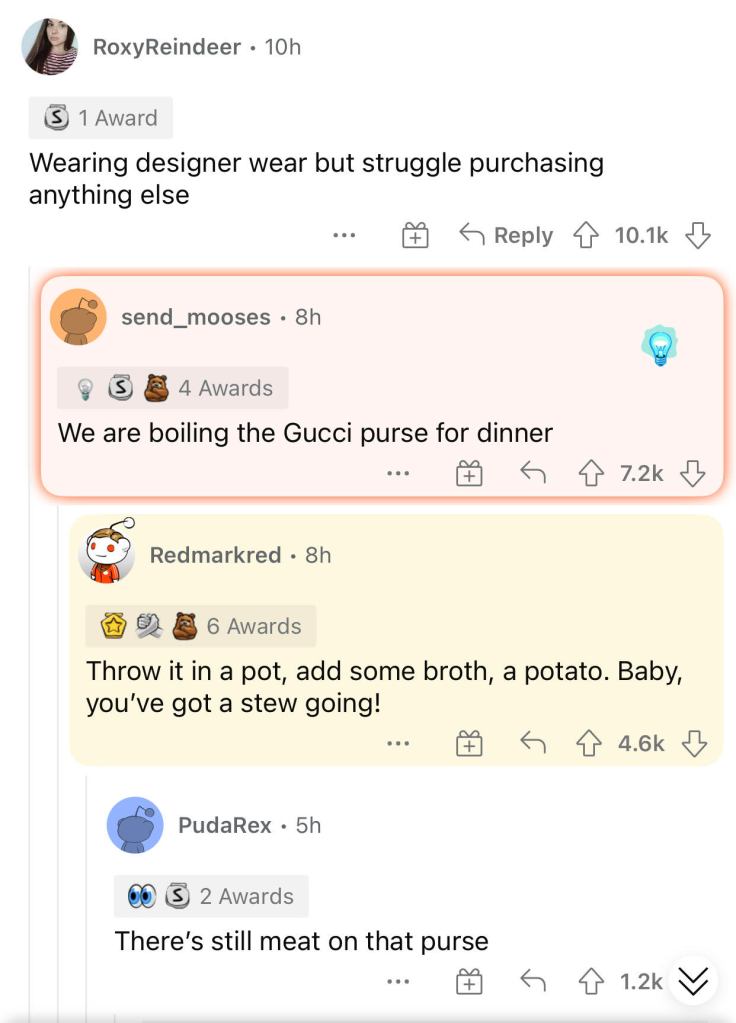

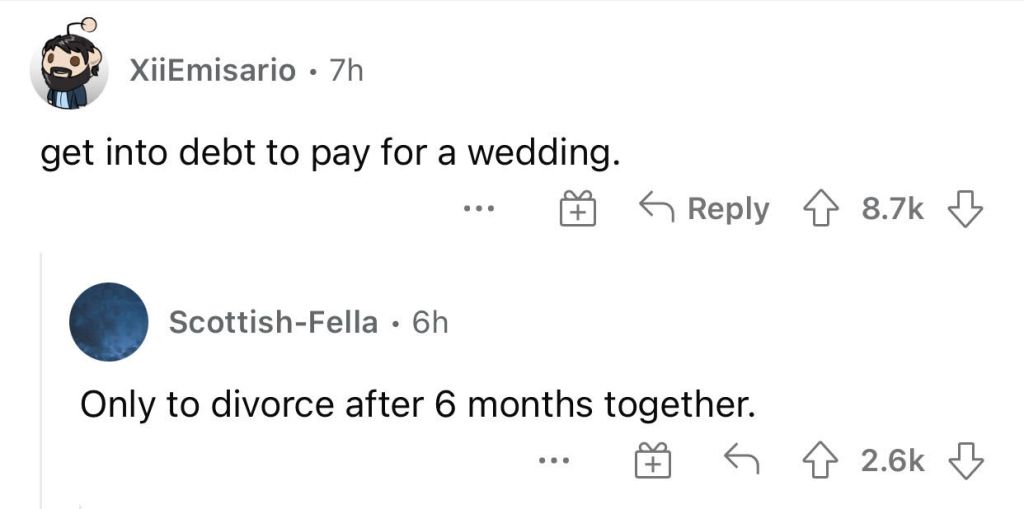

I happened to stumble upon a Reddit thread today. It was titled “What common thing screams “I make poor financial choices?”

I am attaching screenshots below with some personal finance mistakes to ponder upon. Some of the replies are witty. I am including them just for smiles!

Getting another pet when you are not financially ready

Personal Finance Blunders #1

Rolling car payments into your next car

Personal Finance Blunders #2

Buying expensive infant/baby/toddler clothes

Personal Finance Blunders #3

Not living within your means

Personal Finance Blunders #4

Wearing/Owning designer brands but struggling to purchase anything else

Personal Finance Blunders #5A lot of car-related answers!

It is only recently that I came to know about Naval Ravikant.

A popular Indian YouTuber was raving about him in a recent video of his. It led me to this highly popular twitter thread titled “How To Get Rich Without Getting Lucky” and the thought-provoking Joe Rogan episode. I was hooked.

Naval Ravikant is an entrepreneur and angel investor. He had invested in a number of popular startups in Silicon Valley early-on like Twitter and Uber. What makes him different from other businessmen is his thirst for knowledge beyond investing. He is a deep thinker who is intrigued about human psychology and can passionately discuss topics such as meditation, emotional health, happiness and peace. For him, it is not all about money, but he does not dismiss wealth. He believes in a good mix of both, which is refreshing, because we usually see influencers either scorning wealth or being too into it.

Naval Ravikant does not want to monetize his knowledge, because a) he’s already rich b) he says it defeats his purpose of altruism. This makes you want to trust him.

After going through many tweets of his (he is quite popular on Twitter), and the Joe Rogan video, I ended up downloading the free book called “The Almanack of Naval Ravikant” which is a compilation of his best advice and anecdotes.

Here are a few Naval Ravikant quotes that left a mark on me from the book:

Making money is not a thing you do – it’s a skill you learn.

Specific knowledge is found much more by pursuing your innate talents, your genuine curiosity, and your passion. It is not by going to school for whatever is the hottest job; it is not by going into whatever field investors say is the hottest.

The internet enables any niche interest, as long as you’re the best person at it to scale out. And the great news is because every human is different, everyone is the best at something – being themselves.

Escape people through authenticity. Basically, when you are competing with people, it is because you’re copying them. It is because you are trying to do the same thing. But every human being is different. Don’t copy.

The most important skill for getting rich is becoming a perpetual learner. You have to know how to learn anything you want to learn.

Compound interest also happens in your reputation. If you have a sterling reputation and you keep building it for decades upon decades, people will notice. Your reputation will literally end up being thousands or tens of thousands of times more valuable than somebody else who was very talented but is not keeping the compound interest in reputation going.

Knowledge only you know or only a small set of people knows is going to come out of your passions and your hobbies, oddly enough. If you have hobbies around your intellectual curiosity, you’re more likely to develop these passions.

We waste our time with short-term thinking and busywork. Warren Buffett spends a year deciding and a day acting. That act lasts decades.

Value your time at an hourly rate, and ruthlessly spend to save time at that rate. You will never be worth more than you think you’re worth.

Literally, being anti-wealth will prevent you from becoming wealthy, because you will not have the right mindset for it, you won’t have the right spirit, and you won’t be dealing with people on the right level.

The problem is, to win at a status game, you have to put somebody else down. That’s why you should avoid status games in your life—they make you into an angry, combative person. You’re always fighting to put other people down, to put yourself and the people you like up.

Retirement is when you stop sacrificing today for an imaginary tomorrow. When today is complete, in and of itself, you’re retired.

Money is not the root of all evil; there’s nothing evil about it. But the lust for money is bad. The lust for money is not bad in a social sense. It’s not bad in the sense of “you’re a bad person for lusting for money.” It’s bad for you. Lusting for money is bad for us because it is a bottomless pit. It will always occupy your mind. If you love money, and you make it, there’s never enough.

To the extent money buys freedom, it’s great. But to the extent it makes me less free, which it definitely does at some level as well, I don’t like it.

The most common bad advice I hear is: “You’re too young.” Most of history was built by young people. They just got credit when they were older. The only way to truly learn something is by doing it. Yes, listen to guidance. But don’t wait.

Let’s get you rich first. I’m very practical about it because, you know, Buddha was a prince. He started off really rich, then he got to go off in the woods.

It’s only after you’re bored you have the great ideas. It’s never going to be when you’re stressed, or busy, running around or rushed. Make the time.

The smaller the company, the more everyone feels like a principal. The less you feel like an agent, the better the job you’re going to do. The more closely you can tie someone’s compensation to the exact value they’re creating, the more you turn them into a principal, and the less you turn them into an agent.

I am just another person hoping for financial freedom one day.

But since the last few years, I have been enjoying reading about personal finance, researching and then taking action. As mentioned in my previous post, I have no clue where this journey will take me, but it has been an enlightening one so far.

I must have been 10 or 11 when a friend’s father asked a question to a bunch of kids (including me) at a party – “How much of your salary should you save once you start earning?” I remember just staring back at him. I had no clue. To be fair, which 10-11 year old would? Our parents don’t usually ask us such things. He answered “20%” and since then that percentage has stuck in my mind, living rent-free, refusing to leave.

20%. I took this number with me. When I started working, it was the first thing I thought of. Makes me wonder – if only kids were taught personal finance at school. They would grow up to be better at managing money.

I am 36. There are times I wish I had started my journey on learning about personal finance a bit sooner. I try to comfort myself saying I did not have the resources I do now back then. Our resources were our parents, relatives, friends and all those people we regularly interacted with. In short, people who were not financial experts. My 20s and early half of my 30s were mostly spent in a bubble, thinking Fixed Deposits (FDs) are the way to go. When I started researching, all the info I got just blew my mind.

If you are in your 20s, this is the best time to learn about personal finance and invest because there are so many valuable free guides online. Plus, you have age on your side!

It was only recently, in the last couple of years, that I learnt saving your money alone is just not enough. You need to invest as well to create wealth.

Here are a couple of things I have learnt from my personal finance journey so far:

Read books, watch videos, listen to podcasts, read personal accounts on Quora and Reddit.

Diversify not just your investments, but your knowledge sources as well. Get your knowledge on personal finance in various formats. Don’t just stick to one.

Latch on to the things that the different sources keep repeating. I find these repeated pearls of wisdom are of more value and reliability than the things that do not get repeated.

Use social media to gain knowledge. Follow “Personal Finance”, “Investing” topics on Twitter. Related tweets will pop up on your feed. You will find some of the best personal (and honest) anecdotes and tips this way.

If you are on Instagram, search for personal finance pages/experts and follow them. Same for Facebook and any other social media platform.

Start investing in equity as early as you can.

Be patient with your investments. When I started off investing, the value of my portfolio went down considerably, but then picked up in 3 years. My emotions varied from “Did I make the right choice?Maybe I should exit.” when I first started off to “Why didn’t I start this sooner?” after 3 years.

Live below your means. I am trying not to increase my standard of living as my income increases. Instead, I am trying to increase my savings/investments.

20% – always keep this percentage in mind.

Do not trust every advice you see on the Internet (including this post!) – do your own research, and customize your own personal finance itinerary depending on your risk profile. Whatever step you take, make sure you take it as soon as you can after doing a proper research.

You must be logged in to post a comment.